Investing: The Line in the Sand

Sunday, March 23, 2008

It’s pretty easy for us to go through life and not worry about what happens on Wall Street or in the market. We read the headlines, hear of people who have been affected by the turmoil in the markets, but for most of us, all we see are higher gas prices and perhaps, mortgage payments.

By any measure, it’s been an extraordinary week in the markets. And that can be unfortunate – “ for those who worked at Bear Stearns, or for those who have lost jobs or homes – or it can be an opportunity, if you are prepared to take advantage of it.

The Week That Was

So what exactly happened? That’s still a matter of debate in some circles. The Wall Street Journal spared no hyperbole, declaring, “The Week That Shook Wall Street – “ Inside the Demise of Bear Stearns.” Dick Bove, an analyst at Punk, Ziegel, proclaimed, “The Financial Crisis Is Over.” Others were more restrained, writing cautious articles with titles such as “Hitting Bottom?”

For me, I think there are two major things happened this week. The first is that we stopped the “run on the bank” phenomenon. The second is that the Fed found a way to do it without lowering interest rates. Let me explain why these events were so important.

Stopping the Run on the Bank

So let’s start with the first. We all know that banks take our money and lend it out. As a result, if we all went to the bank at the same time and asked for our money back, the bank couldn’t give it to us because they don’t have it. In normal times, we don’t worry about it much. But in times of financial crisis, we start thinking, “Maybe the bank made a bunch of bad loans, and it isn’t going to get back all that money that it lent out.” And so we run to the bank demanding our money back, and by doing so, cause the very disaster we were trying to avoid. The crux of it is, the loans that the bank made might actually be good ones. But it doesn’t matter, because fear by itself is enough to cause the “run on the bank.”

A lot of people will be hurt, and will take a long time to recover from that week. Yet what happened to Bear will, in the long term, be good for the markets.

There’s one other thing to keep in mind about the “run on the bank” phenomenon. It’s not long before people start thinking, “Well, that might not be the only bank in trouble. In fact, if that bank is in trouble, other banks must be in trouble.” And before you know it, the entire system could fall apart.

So that’s what almost happened last week. One day, the CEO of Bear Stearns, Alan Schwartz, was saying that the company had no liquidity problems. A day or two later, Bear was near bankruptcy. By the end of the weekend, the government stepped in and forced the sale of the company for $2 a share (although this may not be the final selling price). Last year, Bear was trading for as much as $165 a share at its high. Wow. I have to admit, I have been surprised by the markets in the last year. But on this headline, I did a double-take. I’d call it a shock.

What happened was that rumor and fear had gripped the markets. Whether Bear had good or bad assets on its books is almost irrelevant now; just the belief that Bear could not handle its obligations was enough to bring it down.

To be fair, there are some technical differences between the “run on a bank” scenario and the Bear Stearns debacle. Bear Stearns isn’t really a commercial bank, it’s an investment bank. So it wasn’t depositors like you and me that were in trouble, but businesses and other banks that trade with Bear. Essentially, nobody would do a deal with Bear, because nobody could be sure that Bear would hold up its end of the bargain. Fear, not necessarily reality, is what destroyed the company.

For the employees and the shareholders of Bear Stearns, we have a tragic and traumatic event. A lot of people will be hurt, and will take a long time to recover from that week. Yet what happened to Bear will, in the long term, be good for the markets. That’s because the Fed was very well aware of what we talked about above – “ that the fear that took down Bear could easily spread to other banks and threaten the entire system. That’s why they stepped in and forced a sale of the company rather than allowing it to go into bankruptcy. In addition, they took the unprecedented step of guaranteeing up to $30 billion of Bear Stearns’ illiquid securities. The government and the Fed basically drew a line in the sand and said they would do whatever it takes to save the system. And they did; they stopped the “run on the bank”.

In our last article, we looked at all the “mini-crisis” that had occurred over the last year. We have been hit by fears that hedge funds would fall apart, and that the malaise would spread throughout the system; that fancy financial instruments and financial structures with acronyms such as SIVs, CDOs and CMOs would cause the fall of banks; or that related parties, such as the mortgage insurers, would take down investors and even local municipalities. In each case, the Fed tried to let the market handle it, but eventually had to step in and lower interest rates. In each case, the market rallied for a very short while, only to run into another crisis that sent stocks down to ever lower levels. Before long, the market was beginning to worry that the Fed was out of tricks in its hat. After all, the problems just kept popping up, and you know, you can only lower rates so far.

A New Tool

This brings us to the other major event that occurred last week: the Fed found a way to inject liquidity into the system without lowering interest rates. Why is this important? Because lowering interest rates has a price: inflation.

Lowering rates “greases the wheels” of the financial system, so to speak. With each rate cut, it becomes more likely that borrowers will borrow and that lenders will lend. In theory, this increased activity spurs the economy and eventually leads to growth. But in the longer term, inflation can take off as well. The Fed has been reluctant to cut rates for exactly this reason.

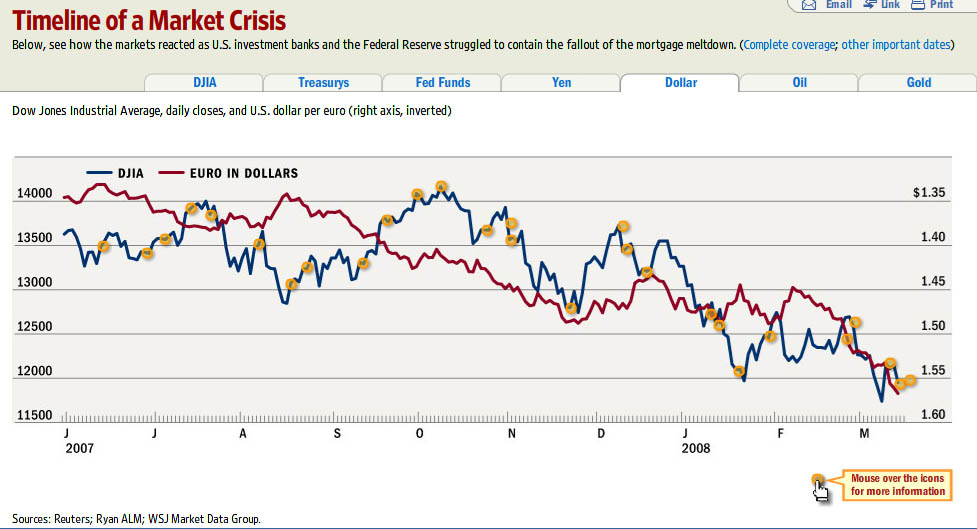

Over the last year or two, the fall in the value of the dollar, the increase in the price of oil, and the increase in the price of gold, have all been due, in part, to the decline in interest rates. Take a look at the following charts from the Wall Street Journal. The first shows the declining Dow, accompanied by falling Federal Funds rate.

Likewise, the dollar has fallen against the Euro in concert.

Meanwhile, the price of oil has risen:

And so has the price of gold.

Last week, the Fed continued to lower interest rates by cutting the Federal Funds rate by 75 basis points and by lowering the discount rate by 100 basis points.

But that was not all that it did. Over the last year, the market has been unwilling to hold the securities of banks and other firms. Creditors feared that these securities were tainted by the mortgage crises. As a result, banks and other companies that borrow to maintain their operations have had a hard time.

This week, the Federal Reserve attacked this problem by agreeing to take on $200 billion of bank securities. This provided liquidity to the banks and allowed them to maintain their operations. Originally, this was for a 28-day period, but the Fed has said that it will continue this program. In addition, the Fed initiated another facility that would allow banks and primary dealers to borrow up to $200 billion at the discount window by providing securities, including AAA asset-backed bonds, as collateral. In other words, the Fed is doing what no one else in the market will: lending directly against securities that others feared would decline in value.

The Fed has taken another ground-breaking step by allowing primary dealers – “ aka investment banks (such as Bear Stearns) – to borrow from the discount window. Traditionally, only commercial banks such as Citigroup were allowed to do so. This week, both Lehman and Goldman borrowed from the window.

The beauty of this solution is that first, it goes directly to the heart of the problem. The Fed is lending and making sure that there is liquidity where others won’t. This will prevent the “run on the bank” because this way, the banks will always have access to funds. Secondly, this tool has less of the inflation causing effects of lowering interest rates. It is no surprise that in the days after these Fed announcements, the price of gold, which was as high as $1,030 an ounce, fell to $920 an ounce by this last Thursday, March 20, 2008. Likewise, oil, which was as high as $111.80 earlier this week, fell to less than $101. Commodities took a hit as well.

I think the Fed is to be congratulated for taking bold and very appropriate action. And it did so by coming up with new, innovative tools to solve the problem.

What Comes Next

This doesn’t mean that the problems are over. Remember that there is still a series of mortgage resets this year that will reduce the value of securities held by many institutions. That means more write-downs and more hits to earnings. But the Fed has managed to remove the fear that the value of stocks could be a bottomless pit. Does anyone doubt now that the Fed will step in if another institution (such as Bear) were to run into problems? Even now, the SEC has staff sitting in the halls of investment banks, going over the books to make sure that these firms have sufficient liquidity.

Does that mean it is time to buy? That we have hit bottom? No one can guarantee that the answer to these two questions is “yes”. I would say that you can start building a position, meaning that you buy some, see how the market does, and buy more if you think the conditions are right. Remember, we have time and there is no rush. While the Fed has stemmed the tide, it doesn’t mean that the storm is over, and the market isn’t about to recover overnight.

Stock Updates

Citigroup. Last fall, I said that sometime in Q1 or Q2 of this year would be the time to buy Citigroup. It is now the end of Q1 and we are in the window. I think that recent events support buying for long-term investors. I will wait a bit longer to see if the market has stabilized, and I expect to start nibbling. Keep in mind that in Q2, I expect Citibank to be hit by another round of writedowns, so the bad news isn’t over by any means. But if you were to look at Citigroup as an investment over the next three years, then buying in the next two quarters is likely to be a very good proposition. I currently have a position in Citigroup.

Goldman Sachs. I sold all of my Goldman stock last year and it’s such a great franchise that I’m always looking for a re-entry point. Goldman has done well in this crisis and has come off year lows in the days following the Fed action. Still, the move happened too fast for me, and I think it will be sometime before all its lines of business are kicking in high gear. In other words, the market turned too fast for me to catch the bottom, and it’s not yet into the next cycle. So I’m holding off buying any for the moment.

US Bancorp. As mentioned in previous articles, I’m a fan of US Bancorp. It’s conservatively managed, has had little exposure to the mortgage crisis, and was basically taken down with the rest of the banking sector. I bought a little in the $31 range, and this week it rose to the $34 range. My only regret is not buying more, and I would recommend buying on any dip.

Huntsman. I wrote about Huntsman as a merger arbitrage play. This week it fell to the mid-$23 range, with a close expected at $28 in the second quarter. I’m long the stock and have my fingers crossed. I may very well buy some more, too.

Altria. By the end of the month, Altria is expected to spin off Philip Morris International. I’ve held onto the stock, and will hold both Altria (the US arm) and Philip Morris International (the international arm) through the spin-off. I think both continue to have strong growth prospects for the long term, and both will have very respectable dividends. Altria remains my largest position.

Boeing. I’ve long been a fan of Boeing but sold all my stock when delays in production were expected. This month, the word is that additional delays are expected. This doesn’t reflect a problem with the company; building a new airplane using a new production process is simply a difficult proposition. Once a delivery is predictable, I would buy the stock again.

Those are the thoughts for the month, until next time, sleep well.

Ming Lo is an actor, director and investor. He has an A.B. from Harvard College, Cum Laude, and an MBA and an MA Political Science from Stanford University. Prior to going into entertainment, Ming worked at Goldman, Sachs & Co. in New York and at McKinsey & Co. in Los Angeles.

All material presented herein is believed to be accurate but we cannot attest to its accuracy. The writings above represent the opinions of the author, and all readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed may change without prior notice. The author may or may not have investments in the stocks or sectors mentioned.

Hi,

Very Good!

Please help me to find a good forex broker.

“If anybody knows about the England Foreign Exchange EFXCO please let me know.

Thanks”

If you’re in uncomfortable position and have no cash to get out from that, you would need to take the personal loans. Because it should aid you unquestionably. I get short term loan every year and feel myself good just because of it.